Your Guide: Healthcare Claims Processing Steps

If you’re an employer who’s trying to contend with excessive healthcare costs, you are not alone! While per-employee medical costs increased by 3.2% in 2022, according to Mercer’s annual survey, health plans are expected to see another sharp increase and rise another 5.6% in 2023.

Needless to say, healthcare has become unconscionably expensive. The increasing costs mean that many employers are looking for cost-saving methods that may result in substantial benefit cuts. Because healthcare benefits are tremendously important to employee retention and recruiting, cutting benefits may not be the best long-term solution.

There is a silver lining: with so many other employers feeling the same pressure, more companies are embracing innovative solutions to help mitigate the costs without sacrificing the quality of employee healthcare.

One such solution addresses the difficulty of navigating complex healthcare claims processing methods. This blog post discusses the common steps in traditional healthcare claims processing and suggests how alternatives to this labyrinthine process can help you save on company healthcare costs.

What Are the Healthcare Claims Processing Steps?

Medical claims look like billing statements, but they are a bit more specific. Healthcare providers send claims to health insurance companies to request reimbursement for medical services. In addition to the coinsurance employers and employees pay—as a percentage of a procedure’s cost—these claims ensure that private insurance companies pay providers as well.

While you may be familiar with sending healthcare claims to a private insurance company, you may be unaware of the process itself. Unfortunately, the path traditional health insurance follows to process claims is needlessly complicated, which leaves room for a rather consequential margin of error.

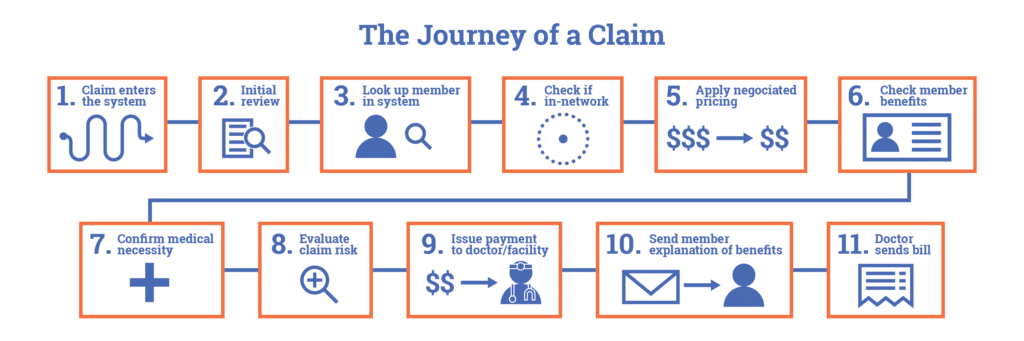

While individual insurance companies may make slight variations to the process, they generally share a similar framework. To help readers better understand this complex system, here are the most common healthcare claims processing steps, including:

- File claim. The first step of the healthcare claims process is submitting a claim, either as a physical copy or digitally. If a hard copy claim is submitted, it must be translated into a digital format.

- Initial review. Once the insurance carrier receives the claim, they review it to ensure it has been filed within an appropriate filing period. Typically, a software algorithm also searches for duplicate charges or inaccurate data.

- Verify member. The insurance carrier verifies member eligibility by checking their system to see if the member has an active insurance plan.

- Verify network. The insurance carrier checks to ensure services on the claim have been performed by a member provider in their healthcare network.

- Apply negotiated price. Insurance companies have contracts with providers in their networks that establish fixed-price discounts. These negotiated rates are applied once the member and network are verified.

- Verify member benefits. One of the lengthiest parts of the process is when the insurance company verifies membership details, like whether the member’s benefits cover the services, which benefits apply where, and what percentage of cost-sharing the member and their employer are responsible for paying.

- Verify medical necessity. Once the member, network, and benefits are verified, the insurance company decides whether the services listed on the claim are necessary for the patient’s medical needs.

- Evaluate claim risk. The company’s software automatically flags claims for potential insurance fraud.

- Issue payment to provider. Having authenticated the validity of the claim, the insurance company sends payment to the provider.

- Communicate Explanation of Benefits (EOB) to members. Members receive an EOB statement—not a bill—that details the total cost of services billed, how much insurance covers, and what they can expect to pay for coinsurance.

- Bill patients and employers for the remainder. If services are performed that insurance does not cover, the patient and employer are responsible for the charges. The provider sends them a bill that usually aligns with the EOB.

Billing Errors: Common, but Unacceptable

As you can see, there are many steps to the healthcare claims process, which results in overly convoluted billing practices. While some redundancies can offer limited reassurances, such complex systems often compound problems that arise from billing errors. When one considers that 80% of all medical bills contain errors, this process only obfuscates underlying issues and makes it more difficult to correct mistakes.

Errors include duplicate charges, medical coding errors, network errors, or “upcoding”—a practice wherein providers intentionally inflate the costs of services and resources to account for a presumed increase in resource requirements.

Each negative billing factor compounds the other; the frequency of mistakes creates even more room for error in an elaborate billing process that seems impenetrable to employers and patients. Insurance companies further amplify the inconvenience of billing rituals and their wake of frustration with a distinct lack of incentive to investigate any discrepancies.

Private insurance companies are only positioned to profit—either because of negotiated provider discounts or from the obligatory charges paid by patients and employers, with or without errors. In addition, expensive fees like premiums and deductibles get paid annually, regardless of whether employees use their medical benefits.

All of these ingredients combine for an all-too-common reality in which employers and patients pay for charges they shouldn’t and insurance companies, serving as middlemen, have little incentive to combat it.

But there’s good news! You don’t have to settle for traditional health insurance companies that pay whatever’s listed on their bills and shift the burden of cost to you. One of the many benefits of leaning on a claims processing expert is that they will scrutinize medical bills and remove any errors that would have been paid—before you pay your bill—which could save you thousands.

6 Degrees Health’s Clean Claim Reviews Deliver Huge Savings

At 6 Degrees Health, we are not an insurance company. Instead, we offer many cost containment solutions designed specifically to help employers combat rising healthcare costs.

Our data-driven approach includes remedies like Clean Claim Reviews, as part of our payment integrity program. This approach provides an in-depth review of medical bills to identify and eliminate all errors or inconsistencies so you only pay the correct amounts. With the experts at 6 Degrees Health in your corner, you could save up to 40% on your annual healthcare spend.

Are you interested in learning more about Clean Claim Reviews or healthcare claims processing steps? Speak to a representative today to find out how 6 Degrees Health can help you realize true cost savings in healthcare.